General Overview

What is ASEAN

ASEAN is the abbreviation for Association of South East Asian Nations, which is a geo political and economic organisation of countries in South East Asia. The organisation was formed on 8th August 1967 consisting of Indonesia, Malaysia, the Philippines, Singapore and Thailand with goals that include economic growth, protection of regional peace and stability and opportunities to discuss differences peacefully. The organisation later included Brunei, Burma (Myanmar), Cambodia, Laos and Vietnam.

ASEAN’s Economy

Altogether the ASEAN countries generate a combined nominal GDP of more than 2 trillion USD as estimated by IMF in 2012, with Indonesia leading the region at 1.2 trillion USD.

| Rank | Country | Nominal GDP (million USD) |

Nominal Per Capita GDP ( USD) |

GDP (PPP) (million USD) |

GDP per capita (PPP) (million USD) |

|---|---|---|---|---|---|

| 1 | Indonesia | 878,198 | 3,592 | 1,216,738 | 4,977 |

| 2 | Thailand | 365,564 | 5,678 | 651,856 | 10,126 |

| 3 | Malaysia | 303,527 | 10,304 | 498,477 | 16,922 |

| 4 | Singapore | 276,520 | 51,162 | 326,506 | 60,410 |

| 5 | Philippines | 250,436 | 2,614 | 424,355 | 4,430 |

| 6 | Vietnam | 138,071 | 1,528 | 320,677 | 3,548 |

| 7 | Burma | 53,140 | 835 | 89,461 | 1,405 |

| 8 | Brunei | 16,628 | 41,703 | 21,687 | 54,389 |

| 9 | Cambodia | 14,241 | 934 | 36,645 | 2,402 |

| 10 | Laos | 9,217 | 1,446 | 19,200 | 3,011 |

International Trade

The ASEAN as a whole is the third most important trading partner for the EU after the US and China.

ASEAN’s Demography

Altogether the population of ASEAN countries totals up to 615.6 million people as estimated by IMF in 2012

| Rank | Country | Population (million) |

|---|---|---|

| 1 | Indonesia | 244.47 |

| 2 | Philippines | 95.80 |

| 3 | Vietnam | 90.39 |

| 4 | Thailand | 64.38 |

| 5 | Burma | 63.67 |

| 6 | Malaysia | 29.46 |

| 7 | Singapore | 5.41 |

| 8 | Cambodia | 15.25 |

| 9 | Laos | 6.38 |

| 10 | Brunei | 0.40 |

General comparison of ASEAN, China, EU and US

- Economy

| Rank | Economy | Nominal GDP (million USD) |

Nominal Per Capita GDP ( USD) |

GDP (PPP) (million USD) |

GDP per capita (PPP) (million USD) |

|---|---|---|---|---|---|

| 1 | European Union | 16,584,007 | 32,518 | 16,092,525 | 32,021 |

| 2 | United States | 15,684,750 | 49,922 | 15,684,750 | 49,922 |

| 3 | People's Republic of China | 8,227,037 | 6,076 | 12,405,670 | 9,162 |

| 4 | ASEAN | 2,305,542 | 3,745 | 3,605,602 | 5,857 |

- Demography

| Rank | Economy | Population (million) |

|---|---|---|

| 1 | People's Republic of China | 1,354.04 |

| 2 | ASEAN | 615.60 |

| 3 | European Union | 502.56 |

| 4 | United States | 314.18 |

Automotive Industry in ASEAN Countries

Automotive Sales in ASEAN Countries

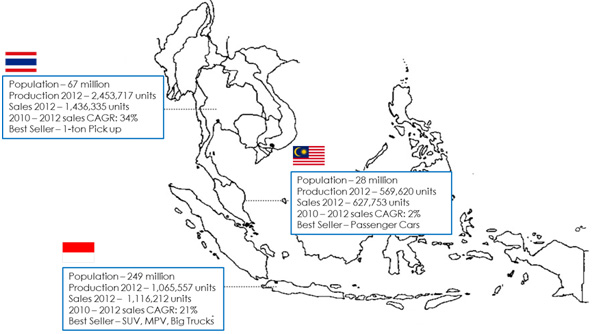

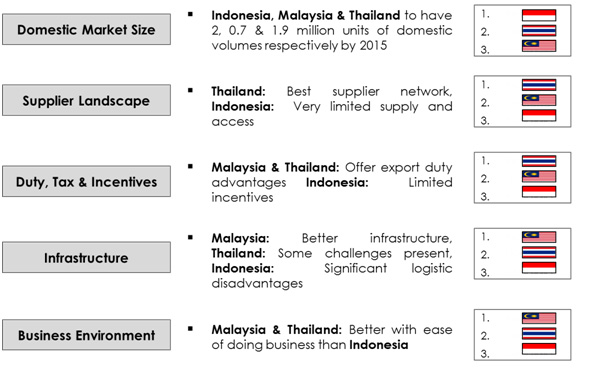

The top three markets in ASEAN for commercial and passenger vehicles are Thailand, Indonesia and Malaysia. In 2012, 1.4 million, 1.1 million and 0.6 million vehicles were sold in Thailand, Indonesia and Malaysia respectively. Together these three markets account for 92% of the vehicle sales in the ASEAN region.

Different types of vehicles are popular in different countries. For example the best seller in Thailand is 1 ton pickup trucks. The best sellers in Indonesia are SUV, MPV and big trucks whereas; the best sellers in Malaysia are passenger cars.

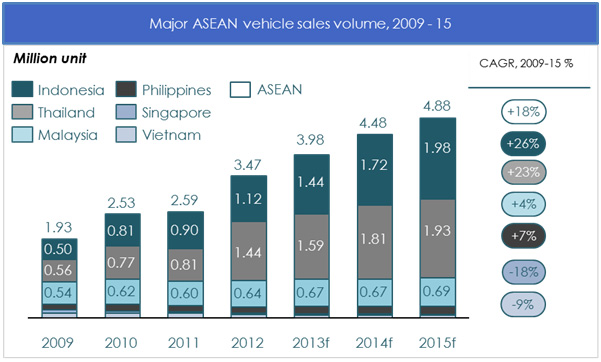

Deutsche Bank estimated that the unit vehicle sales annual growth rate would be 10% on average between 2010 and 2015 resulting in approximately 2.7 million cars sold each year on average in the ASEAN region. It also predicted that the annual growth rate of unit vehicle sales would decline to 7% by 2020 but still resulting in more than 3.7 million cars sold each year on average by that time.

In terms of dollar amount, the total number of automotive sales in the ASEAN countries was estimated to be 63 billion in 2012.

While the largest market in ASEAN at the moment is Thailand, Indonesia is forecasted to be the largest market in the region by 2015.

Major ASEAN Vehicle Sales Volume, 2009 – 2015 (forecast)

| Country | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 |

|---|---|---|---|---|---|---|---|

| Vietnam | 119459 | 112224 | 110938 | 80487 | 75657.78 | 71118.31 | 66851.21 |

| Singapore | 79503 | 51891 | 39570 | 37247 | 32404.89 | 28192.25 | 24527.26 |

| Philippines | 132444 | 168496 | 141616 | 156649 | 168075.5 | 180335.5 | 193489.7 |

| Malaysia | 544000 | 616000 | 598000 | 640000 | 666000 | 672000 | 690000 |

| Thailand | 560000 | 814000 | 805000 | 1440000 | 1591000 | 1806000 | 1932000 |

| Indonesia | 496000 | 770000 | 897000 | 1120000 | 1443000 | 1722000 | 1978000 |

ASEAN Vehicle, Motorcycles and Scooter Sales Statistics

The following is statistical data from the ASEAN Automotive Federation (AAF)

- 2012 Sales - Vehicles Sales in ASEAN

| Country | Passenger Vehicles | Commercial Vehicles | 2012 | 2011 | Variance(%) |

|---|---|---|---|---|---|

| Brunei | 17,854 | 780 | 18,634 | 14,555 | 28% |

| Indonesia | 780,767 | 335,445 | 1,116,212 | 894,164 | 25% |

| Malaysia | 552,189 | 75,564 | 627,753 | 600,123 | 5% |

| Philippines | 48,328 | 108,326 | 156,654 | 141,616 | 11% |

| Singapore | 32,724 | 4,523 | 37,247 | 39,570 | -6% |

| Thailand | 694,234 | 742,101 | 1,436,335 | 794,081 | 81% |

| Vietnam | 43,692 | 36,761 | 80,453 | 109,660 | -27% |

| TOTAL | 2,169,788 | 1,303,500 | 3,473,288 | 2,593,769 | 34% |

- Motorcycles & Scooters Sales in ASEAN

| Country | 2012 | 2011 | Variance(%) |

|---|---|---|---|

| Indonesia | 7,141,586 | 8,043,535 | -11% |

| Malaysia | 537,753 | 494,586 | 9% |

| Philippines | 702,599 | 731,130 | -4% |

| Singapore | 9,923 | 8,046 | 23% |

| Thailand | 2,130,067 | 2,007,383 | 6% |

| TOTAL | 10,521,928 | 11,284,680 | -7% |

- 2011 Sales - Vehicles Sales in ASEAN

| Country | Passenger Vehicles | Commercial Vehicles | 2012 | 2011 | Variance(%) |

|---|---|---|---|---|---|

| Brunei | 13,472 | 1,083 | 14,555 | 13,589 | 7% |

| Indonesia | 601,945 | 292,219 | 894,164 | 764,710 | 17% |

| Malaysia | 535,113 | 65,010 | 600,123 | 605,156 | -1% |

| Philippines | 44,862 | 96,754 | 141,616 | 168,490 | -16% |

| Singapore | 33,493 | 6,077 | 39,570 | 51,891 | -24% |

| Thailand** | 360,441 | 433,640 | 794,081 | 800,357 | -1% |

| Vietnam | 64,505 | 45,155 | 109,660 | 111,737 | -2% |

| TOTAL | 1,653,831 | 939,938 | 2,593,769 | 2,515,930 | 3% |

** For Thailand, sales data for passenger cars will not include MERCEDES BENZ, BMW, MINI and VOLVO from November 2011 onwards

- Motorcycles & Scooters Sales in ASEAN

| Country | 2012 | 2011 | Variance(%) |

|---|---|---|---|

| Indonesia | 8,006,293 | 7,395,390 | 8% |

| Malaysia | 498,076 | 467,941 | 6% |

| Philippines | 762,947 | 813,361 | -6% |

| Thailand | 2,043,039 | 2,024,599 | 1% |

| TOTAL | 11,284,680 | 10,480,946 | 8% |

- 2010 Sales - Vehicles Sales in ASEAN

| Country | Passenger Vehicles | Commercial Vehicles | 2010 | 2009 | Variance(%) |

|---|---|---|---|---|---|

| Brunei | 12,549 | 1,040 | 13,589 | 12,365 | 10% |

| Indonesia | 541,475 | 223,235 | 764,710 | 483,550 | 58% |

| Malaysia | 543,594 | 61,562 | 605,156 | 536,905 | 13% |

| Philippines | 58,691 | 109,799 | 168,490 | 132,444 | 27% |

| Singapore | 47,273 | 4,618 | 51,891 | 79,503 | -35% |

| Thailand | 346,644 | 453,713 | 800,357 | 548,871 | 46% |

| Vietnam | 58,105 | 53,632 | 111,737 | 119,460 | -6% |

| TOTAL | 1,608,331 | 907,599 | 2,515,930 | 1,913,098 | 32% |

- Motorcycles & Scooters Sales in ASEAN

| Country | 2010 | 2009 | Variance(%) |

|---|---|---|---|

| Indonesia | 7,398,644 | 5,881,777 | 26% |

| Malaysia | 468,175 | 432,683 | 8% |

| Philippines | 759,849 | 636,889 | 19% |

| Singapore | 8,281 | 8,883 | -7% |

| Thailand | 1,845,997 | 1,535,461 | 0 |

| TOTAL | 10,480,946 | 8,495,693 | 23% |

ASEAN Vehicle, Motorcycles and Scooter Production Statistics

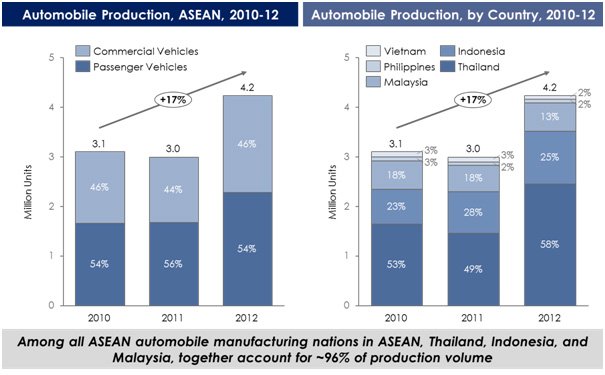

Thailand, Indonesia and Malaysia are not only the largest markets in the ASEAN region but also the major producers of vehicles. Together they account for more than 96% of motor vehicle output in the region.

- Automobile Production in ASEAN by Type

| Type | 2010 | 2011 | 2012 |

|---|---|---|---|

| Passenger Vehicles | 1.663476 | 1.674081 | 2.278573 |

| Commercial Vehicles | 1.438694 | 1.320548 | 1.959407 |

- Automobile Production in ASEAN Country

| Country | 2010 | 2011 | 2012 |

|---|---|---|---|

| Thailand | 1.645304 | 1.457795 | 2.453717 |

| Indonesia | 0.702508 | 0.837948 | 1.065557 |

| Malaysia | 0.567715 | 0.533515 | 0.56962 |

| Philippines | 0.080477 | 0.064906 | 0.075413 |

| Vietnam | 0.106166 | 0.100465 | 0.073673 |

Deutsche Bank predicted that 6 million cars and trucks would be manufactured in the region in 2020.

Production Statistics

The following is statistical data from the ASEAN Automotive Federation (AAF)

- 2012 Production - Vehicles Production in ASEAN

| Country | Passenger Vehicles | Commercial Vehicles | 2012 | 2011 | Variance(%) |

|---|---|---|---|---|---|

| Indonesia | 743,501 | 322,056 | 1,065,557 | 837,948 | 27% |

| Malaysia | 509,621 | 59,999 | 569,620 | 533,515 | 7% |

| Philippines | 26,340 | 49,073 | 75,413 | 64,906 | 16% |

| Thailand | 957,623 | 1,496,094 | 2,453,717 | 1,457,795 | 68% |

| Vietnam | 41,488 | 32,185 | 73,673 | 100,465 | -27% |

| TOTAL | 2,278,573 | 1,959,407 | 4,237,980 | 2,994,629 | 42% |

- Motorcycles & Scooters Production in ASEAN

| Country | 2012 | 2011 | Variance(%) |

|---|---|---|---|

| Indonesia | 7,079,721 | 8,006,293 | -12% |

| Malaysia | 543,088 | 498,076 | 9% |

| Philippines | 588,292 | 762,947 | -23% |

| Thailand | 2,606,161 | 2,043,039 | 28% |

| TOTAL | 10,817,262 | 11,310,355 | -4% |

- 2011 Production - Vehicles Production in ASEAN

| Country | Passenger Vehicles | Commercial Vehicles | 2011 | 2010 | Variance(%) |

|---|---|---|---|---|---|

| Indonesia | 561,863 | 276,085 | 837,948 | 702,508 | 19% |

| Malaysia | 488,261 | 45,254 | 533,515 | 567,715 | -6% |

| Philippines | 24,591 | 40,315 | 64,906 | 80,477 | -19% |

| Thailand | 537,987 | 919,808 | 1,457,795 | 1,645,304 | -11% |

| Vietnam | 61,379 | 39,086 | 100,465 | 106,166 | -5% |

| TOTAL | 1,674,081 | 1,320,548 | 2,994,629 | 3,102,170 | -3% |

- Motorcycles & Scooters Production in ASEAN

| Country | 2011 | 2010 | Variance(%) |

|---|---|---|---|

| Indonesia | 8,006,293 | 7,395,390 | 8% |

| Malaysia | 498,076 | 467,941 | 6% |

| Philippines | 762,947 | 813,361 | -6% |

| Thailand | 2,043,039 | 2,024,599 | 1% |

| TOTAL | 11,310,355 | 10,701,291 | 6% |

- 2010 Production - Vehicles Production in ASEAN

| Country | Passenger Vehicles | Commercial Vehicles | 2010 | 2009 | Variance(%) |

|---|---|---|---|---|---|

| Indonesia | 496,524 | 205,984 | 702,508 | 464,816 | 51% |

| Malaysia | 522,568 | 45,147 | 567,715 | 489,269 | 16% |

| Philippines | 33,161 | 47,316 | 80,477 | 62,523 | 29% |

| Thailand | 554,387 | 1,090,917 | 1,645,304 | 999,378 | 65% |

| Vietnam | 56,836 | 49,330 | 106,166 | 107,760 | -1% |

| TOTAL | 1,663,476 | 1,438,694 | 3,102,170 | 2,123,746 | 46% |

- Motorcycles & Scooters Production in ASEAN

| Country | 2010 | 2009 | Variance(%) |

|---|---|---|---|

| Indonesia | 7,395,390 | 5,884,021 | 26% |

| Malaysia | 467,941 | 436,430 | 7% |

| Philippines | 813,361 | 634,032 | 28% |

| Thailand | 2,024,599 | 1,634,113 | 24% |

| TOTAL | 10,701,291 | 8,588,596 | 25% |

Competitive Landscape

Japanese players have been dominating the ASEAN automotive industries for as long as anyone could remember. They have been solidly occupying the largest market shares or the second largest market shares in the three largest markets in ASEAN.

To give an illustration of how dominant the Japanese players are in Indonesia, let us take a look at Toyota Motor. Toyota Motor which has been in Indonesia for 40 years has 450 dealerships and a market share of 54%. In contrast, General Motors which has been in Indonesia even longer, since 1938, only has 34 dealerships and less than 1% market share.

Toyota Group together with its affiliates and partners now sells half a million cars annually in Indonesia, which is approximately the size of the whole automotive market sales in the whole country of Malaysia in 2012. Nissan Motor Co’s Chief Operating Officer has been quoted calling Indonesia as a “Toyota Republic”. Being a Japanese brand, this goes to show how dominant Japanese players are in Indonesia and hence ASEAN as it is forecasted to be the largest market in the region in the near future.

Automotive Production Capacity in ASEAN - Forecast

The lucrative automotive sales market in the ASEAN region as reflected by the forecasted significant increase in vehicle demand in the ASEAN countries has prompted leading players in the industry to either expand production capacity or open new manufacturing plants in the region.

In 2012 Toyota announced that it would invest an additional $200 million beyond expansion plans announced the previous year, lifting its Indonesia capacity to 230,000 vehicles annually by 2014. This would more than double today's output.

After leaving the country seven years ago, GM recently, in 2013, invested 150 million USD to reactivate a plant for producing seven-seat van in Indonesia. The plant is expected to produce 40,000 vehicles annually both for the domestic and export market.

In 2012 Ford opened a $450 million plant in Thailand with an output capacity of 150,000 cars per year to meet rising demand in neighbouring countries.Ford’s South East Asia operation recorded a 90% growth in sales in Indonesia in 2012. Peter Fleet, considered the low level of car ownership in Indonesia along with the growing GDP per capita a strong indication of a take-off point. “This is going to be a period of unprecedented growth in Indonesia" said the president of the South East Asia operations.

China's Zhejiang Geely Holding Group Co. is also looking to expand its vehicle-assembly capacity in Indonesia.

South Korea's Hyundai Motor Co. who expects its sales to climb around 35% considers building a factory as a move to upgrade from the current assembly facility in Indonesia as reported by Jongkie Sugiarto, president director of PT Hyundai Mobil Indonesia.

Suzuki Motor announced expansion plan that would almost double its capacity in Indonesia to manufactures 150,000 four-wheeled vehicles annually. It will spend $780 million for this. Suzuki is also negotiating tax incentives with the Indonesian government that would allow it to produce eco-friendly cars in Indonesia.

Bosch, the leading global supplier of technology and services has announced plans in 2013 to establish its first manufacturing facility in Indonesia. The facility which would be located in the greater Jakarta area and commence production in 2014 will manufacture automotive products primarily for Japanese automakers in Indonesia. The company plans to invest 10 million euros and employ more than 120 people in the next three years.

Nissan Motor and Daihatsu Motor are planning to expand capacity as well. And the list goes on.

Different dynamics at the three largest automotive markets in ASEAN

Automotive Spare Parts in ASEAN- Aftermarket analysis

The Philippines

The Philippines are not among the top 3 automotive markets in ASEAN but it is worth mentioning as it is poised to become the largest manufacturer of automobile parts, specifically transmission assemblies. It has recently beaten Japan in exporting vehicle transmission assemblies to the ASEAN region. Japanese companies operating in the Philippines which include Toyota, Mitsubishi and Isuzu export approximately $3.5 billion worth of spare parts compared to Japan’s $1.1 billion annually.

The Philippines account for ~25% of vehicle parts exported to the ASEAN region, and nearly all of them are accounted for transmission assemblies.

Other signs that the Philippines is becoming the manufacturing hub of transmission assemblies include the fact that three of the largest Japanese automotive manufacturer have been heavily active in producing these transmission assemblies in the Philippines.

Indonesia

Two of the largest manufacturers and distributors of automotive components in Indonesia are PT Astra Otoparts, a subsidiary of PT Astra International and PT Indomobil Sukses International. PT Astra Otoparts is considered to be the largest as it supplies automotive components for Toyota and Daihatsu which holds the largest and second largest market shares in Indonesia respectively. PT Astra Otoparts distributes component for Toyota, Daihatsu, Isuzu, UD Trucks, Peugeot, BMW, and Honda brands whereas PT Indomobil Sukes International distributes components for Audi, Foton, Great Wall, Hino, Kalmar, Liugong, Manitou, Nissan, Renault, Renault Trucks, Suzuki, Volkswagen, Volvo, Volvo Trucks and Mack Trucks brand.

Comparison of Automotive Industry in ASEAN with that of China, EU and US

Vehicle population (numbers are estimates for 2012)

EU: ~260 million units

US: ~250 million units

China: ~60 million units

ASEAN: ~30 million units

Vehicle ownership density (estimates for 2012)

US: ~800 vehicles per 1000 inhabitants

EU: ~500 vehicles per 1000 inhabitants

China: ~50 vehicles per 1000 inhabitants

ASEAN: ~40 vehicles per 1000 inhabitants

The relatively much smaller number in ASEAN countries potentially indicate a much pent-up demand yet to be tapped.

New vehicle sales (estimates for 2012)

US: ~14.5 million new vehicles

EU: ~12 million new vehicles

China: ~15 million new vehicles

ASEAN: ~ 3.5 million new vehicles

Automotive Brands preference and market leaders in ASEAN, EU, US & China

China: American brands dominate.

Popular brands: GM (14.7% market share in 2012), Volkswagen AG (14.6% market share in 2012), Ford. Western brands are more popular than local ones due to the low quality perception of cars produced by local companies.

ASEAN: Japanese brands dominate.

Popular brands: Toyota, Honda, Mitsubishi.

Except in Malaysia where Japanese brands take 25% of the market share, in Indonesia and Thailand Japanese brands take close to 90% of the market shares.

EU: European brands dominate.

Popular brands: Volkswagen (25.7% market share in 2012 from 23.7%), Peugeot (10.9% from 11.7%), Vauxhall/Opel (6.9% in 2012).

Daimler AG (5.7% in 2012 from 5.2%), Fiat (6.1% from 6.3%), Renault (8.6% from 10.6%), Ford (6.5% in June 2013)

US: American brands dominate the market.

Popular brands: Detroit/Buick, Cadillac, Chevrolet, Chrysler, Dodge, Ford, GMC, Jeep, Lincoln, and Ram

American brands dominate while Japanese brands follow in second. 2012 data shows that in 2012 American brands, Japanese brands, European brands account for 44.7% account for 36.9%, account for 9.5% and Korean brands account for the rest 8.9%

Analysis and potential implication – Japanese automotive players dominate

Japanese cars dominate the ASEAN market potentially due to the following reasons:

- Japanese cars have a reputation for reliability, which allow second hand cars of these brands able to maintain higher prices than comparable cars. This is true even in the US market.

- Lower import tariff for cars coming from Japan

- The fact that smaller Japanese cars fit better in ASEAN’s relatively smaller roads

- Early mover advantage of Japanese auto makers who moved into the ASEAN market before most other car makers. These automakers have also stuck it out through the Asian financial crisis and other economic and political instability, increasing consumers’ familiarity with their product ranges over time.

In general, Japanese cars have superior intrinsic values. Their reputation for quality and reliability makes it easy for various international markets to accept them. What make them less well received in certain countries are other reasons such as political or social reasons instead of reasons related to the intrinsic values of the cars themselves.

For example, in the case of China, consumers who generally pay high attention to the value to price ratio would generally welcome Japanese cars that are generally optimally priced if not due to political and social tensions between the two countries regarding the Senkaku or Diaoyu island dispute, where the two countries claim for ownership.

In the case of the US, the high quality of Japanese cars has earned them their esteemed second place in terms of the US market share. The reason why a considerable number of Americans still prefers American brands are more due to the sense of nationalism to support the local automotive industry, which indeed is essential to the whole American economy. These consumers wanted to support job creations and job preservations in the US automotive industry. Putting this aside, a sizable number of American consumers consider foreign cars—especially Japanese cars—to be more superior in terms of price, mileage, gas efficiency and reliability compared to local ones albeit these foreign cars are locally assembled. Such sentiment and perception are not uncommon in the US market.

Source: ICIS, National Auto Association

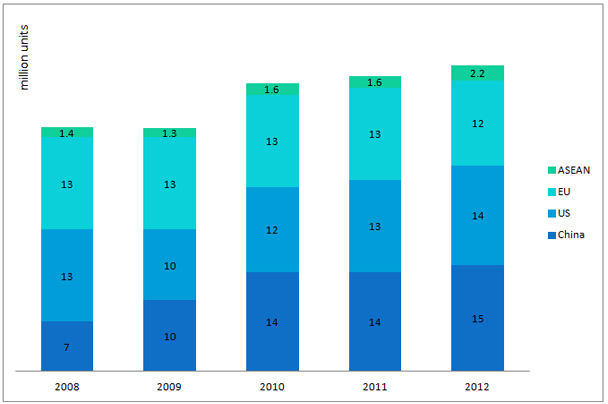

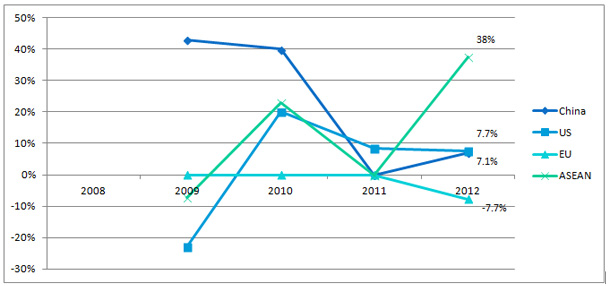

But growth is seen the fastest in ASEAN followed by China. Meanwhile, the EU market is seeing a decline in total market size of passenger cars

Source: ICIS, National Auto Association

Sources:

Shirouzu, Norihiko, “GM Takes on the Toyota Republic”, Jakarta Globe, June 2013